Understanding Cash Value in Life Insurance

- Amber. C

- Feb 2

- 4 min read

Cash value is one of the most misunderstood aspects of life insurance. Some people assume it works like a savings account, while others believe it guarantees strong investment returns. In reality, cash value serves a very specific role within certain types of life insurance policies — and understanding that role is essential.

This guide explains what cash value is, how it works, and what it can (and cannot) be used for.

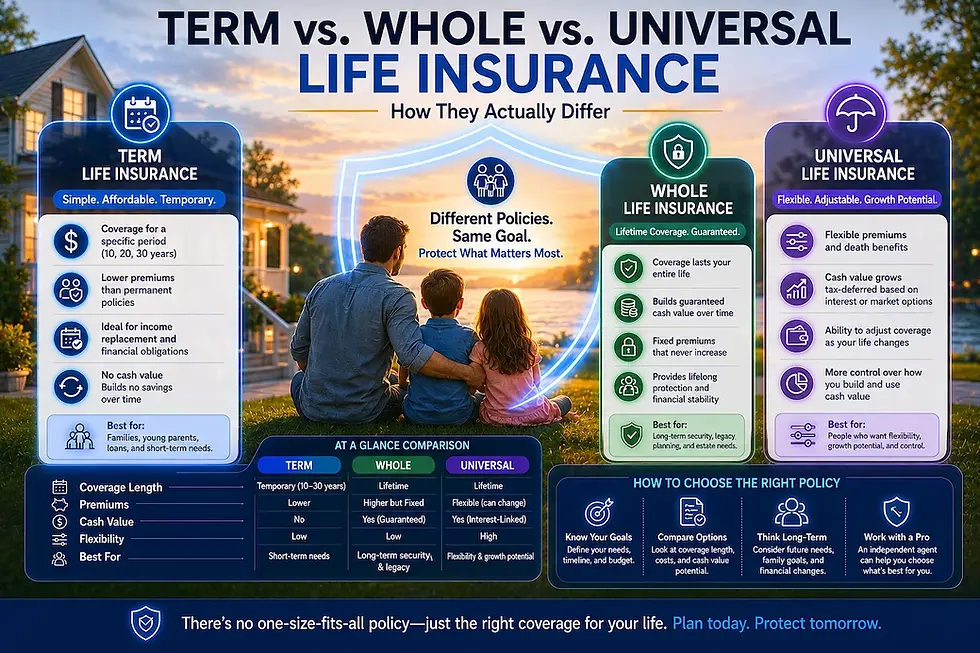

What Cash Value Is

Cash value is a component found in permanent life insurance policies, such as whole life and universal life insurance. It represents a portion of the premiums paid that accumulates inside the policy over time.

Term life insurance does not have cash value.

Cash value exists alongside the death benefit and grows according to the rules set by the policy.

When Cash Value Actually Matters (and When It Doesn’t)

Cash value life insurance isn’t automatically better or worse than term life insurance — it depends on why you’re buying coverage in the first place.

Cash value tends to matter more when:

You expect to keep the policy long-term (10+ years)

You want the option to borrow against the policy later

You’re using life insurance as part of a broader financial plan

Cash value usually matters less when:

You only need coverage for a specific time period

Your main goal is income replacement at the lowest cost

You don’t plan to access the policy while you’re alive

Understanding this distinction helps avoid paying for features you may never use.

How Cash Value Builds Over Time

Cash value growth is not immediate. In the early years of a policy, a significant portion of premiums goes toward:

Policy expenses

Insurance costs

Administrative fees

As the policy matures, cash value typically begins to grow more noticeably.

The rate and structure of growth depend on the type of policy:

Whole life policies usually grow at a guaranteed rate

Universal life policies grow based on interest rates or indexes, depending on design

Real-World Example: Using (and Not Using) Cash Value

Consider two people buying life insurance at age 35:

Person A chooses a permanent life policy and builds cash value over time. At age 50, they borrow against the policy to cover a temporary income gap after changing careers.

Person B chooses term life insurance, pays lower premiums, and invests the difference elsewhere. They never need to borrow against a policy but maintain coverage while their family depends on their income.

Neither choice is universally right or wrong — the difference comes down to how the policy fits into each person’s financial situation.

What Cash Value Can Be Used For

Cash value is not just a number on a statement — it can be accessed in certain ways.

Policy Loans

Many policies allow the policyholder to borrow against the cash value.

Key points:

Loans are not taxable if structured properly

Interest is charged by the insurer

Unpaid loans reduce the death benefit

Withdrawals

Some policies allow withdrawals from the cash value.

Important considerations:

Withdrawals may reduce the death benefit

Excess withdrawals can cause a policy to lapse

Tax treatment depends on policy structure

Premium Payments

In some cases, cash value can be used to help pay premiums.

This can be useful later in the policy’s life, but it requires careful management to avoid unintended consequences.

What Cash Value Is Not

Cash value is often misunderstood as an investment or savings account. It’s important to understand its limitations.

Cash value is not:

A high-yield investment

Fully liquid without consequences

Guaranteed to grow quickly

Separate from the life insurance policy

Its purpose is to support the policy — not replace traditional savings or investment strategies.

How Cash Value Affects Policy Cost

Permanent life insurance policies cost more than term life insurance in part because of the cash value component.

Premiums are higher because they fund:

Lifetime coverage

Policy guarantees

Cash value accumulation

Understanding this trade-off helps explain why permanent policies are structured differently from term policies.

Common Cash Value Misunderstandings

Some common assumptions include:

Cash value can be accessed freely at any time

Cash value equals the death benefit

Cash value growth is always guaranteed

Cash value performs like market investments

These misunderstandings often lead to unrealistic expectations.

Why These Misunderstandings Matter

These assumptions often lead people to choose policies that don’t match their actual needs.

For example:

Expecting fast cash value growth can result in frustration during the early years of a policy.

Treating policy loans as “free money” can unintentionally reduce the payout beneficiaries receive.

Assuming all permanent policies work the same way can cause cost and performance surprises later.

Understanding these limits helps set realistic expectations before choosing a policy.

How Cash Value Fits Into a Broader Plan

Cash value can play a role in long-term planning, but it works best when it aligns with specific goals.

It may be used to:

Provide policy flexibility

Support long-term coverage needs

Offer controlled access to funds under certain conditions

Its usefulness depends on how the policy is structured and maintained over time.

Key Takeaways

Cash value exists only in permanent life insurance

Growth depends on policy type and structure

Loans and withdrawals affect the death benefit

Cash value supports the policy, not replaces investments

Understanding limits prevents costly mistakes

Cash value is a tool within life insurance — not a shortcut to savings or investing. When understood correctly, it helps explain why permanent policies are designed the way they are.

Check out our Amazing!

Comments