Term vs. Whole vs. Universal Life Insurance: How They Actually Differ

- Amber. C

- Feb 1

- 3 min read

Life insurance is often discussed as if it’s a single product, but in reality there are several distinct types — each designed for different goals, time horizons, and financial situations.

The three most common types are term life, whole life, and universal life insurance.

This guide explains how each type works, how they differ, and how to think about them in practical terms.

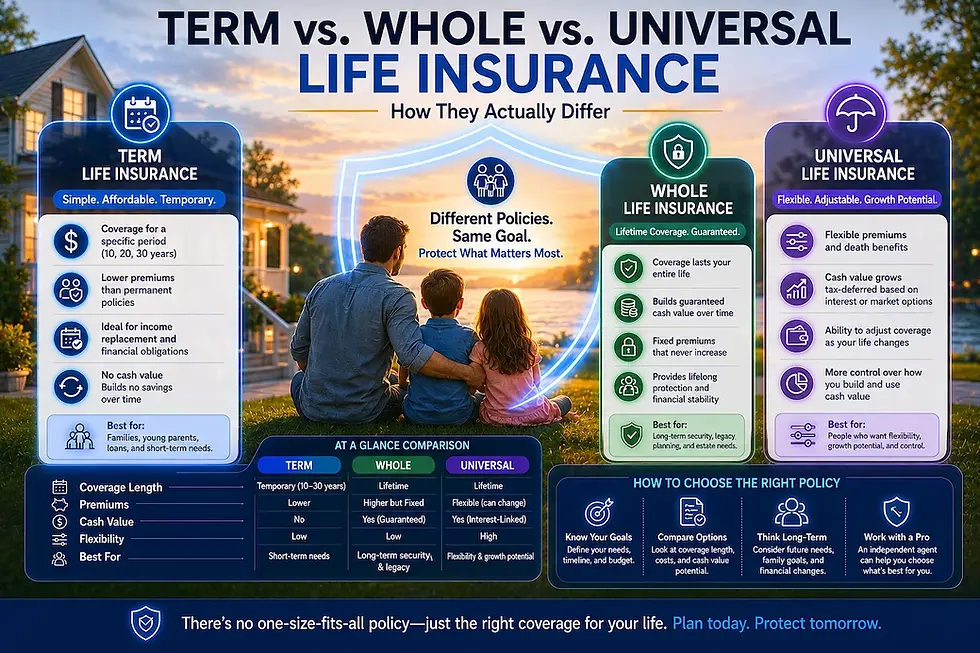

What Term Life Insurance Is

Term life insurance provides coverage for a specific period of time, such as 10, 20, or 30 years.

If the insured person dies during the term, the policy pays a death benefit to the beneficiaries. If the term expires and the insured is still living, the policy ends unless it is renewed or converted.

Key characteristics of term life insurance:

Coverage lasts for a set period

No cash value component

Generally lower premiums

Designed for temporary financial needs

Term life insurance is often used to cover income replacement, mortgages, or other obligations that decrease over time.

What Whole Life Insurance Is

Whole life insurance is a form of permanent life insurance, meaning it is designed to last for the insured’s entire lifetime, as long as premiums are paid.

In addition to a death benefit, whole life insurance includes a cash value component that grows over time at a rate defined by the policy.

Key characteristics of whole life insurance:

Lifetime coverage

Fixed premiums

Guaranteed cash value growth

More expensive than term life

Whole life insurance is typically used when long-term coverage and predictability are priorities.

What Universal Life Insurance Is

Universal life insurance is also a type of permanent life insurance, but it offers more flexibility than whole life.

Universal life policies allow policyholders to adjust premiums and death benefits within certain limits. Cash value growth is tied to interest rates or indexes, depending on the policy type.

Key characteristics of universal life insurance:

Lifetime coverage

Flexible premiums

Adjustable death benefit

Cash value growth varies by policy design

Universal life insurance is often used when flexibility is more important than fixed guarantees.

Key Differences Between Term, Whole, and Universal Life

Coverage Duration

Term: Temporary

Whole: Lifetime

Universal: Lifetime

Cash Value

Term: None

Whole: Guaranteed growth

Universal: Variable or interest-based growth

Cost

Term: Lowest initial cost

Whole: Higher, fixed premiums

Universal: Varies based on funding and structure

Flexibility

Term: Limited

Whole: Minimal

Universal: High

How People Actually Choose Between These Policies

In practice, most people don’t choose between term, whole, and universal life by comparing features alone. The decision usually starts with why coverage is being purchased.

Term life is commonly chosen when:

Coverage is needed for a defined time period

The primary goal is income replacement

Budget flexibility is important

Whole life is commonly chosen when:

Coverage is intended to last indefinitely

Predictable premiums and guarantees matter

The policy is part of a long-term financial plan

Universal life is commonly chosen when:

Flexibility in premiums or death benefits is a priority

Cash value growth is a consideration

Ongoing policy monitoring is acceptable

These patterns help explain how each policy type is typically used, rather than suggesting that one option is universally better than another.

How to Think About Choosing Between Them

The “best” type of life insurance depends on why the coverage is needed.

Temporary needs often align with term life

Long-term or estate-related needs may point toward permanent coverage

Flexibility and long-term planning considerations can make universal life appealing

Understanding how each policy works is more important than focusing on labels or assumptions.

Common Mistakes When Comparing Life Insurance Types

Comparing life insurance options can be misleading when differences in structure are overlooked.

Common mistakes include:

Focusing only on monthly cost without considering how long coverage lasts

Assuming cash value works the same way across policies

Comparing policies without aligning them to the underlying need

Understanding these distinctions helps prevent confusion when reviewing policy options or comparing quotes.

Key Takeaways

Term life is temporary and straightforward

Whole life offers lifetime coverage with guarantees

Universal life prioritizes flexibility

Each type serves different financial purposes

Comparing structure matters more than comparing names

Life insurance works best when it aligns with actual needs, not just general recommendations.

Check out our Amazing!

Comments