Term vs. Whole Life Insurance: How People Actually Decide

- Amber. C

- Dec 20, 2025

- 3 min read

Life insurance decisions are often presented as a simple comparison between term and whole life policies. In practice, the choice is rarely made on features alone. Most people decide based on timing, financial pressure, family responsibilities, and their tolerance for long-term commitments. Understanding how people actually arrive at this decision helps clarify why neither option is universally better, despite how the debate is often framed.

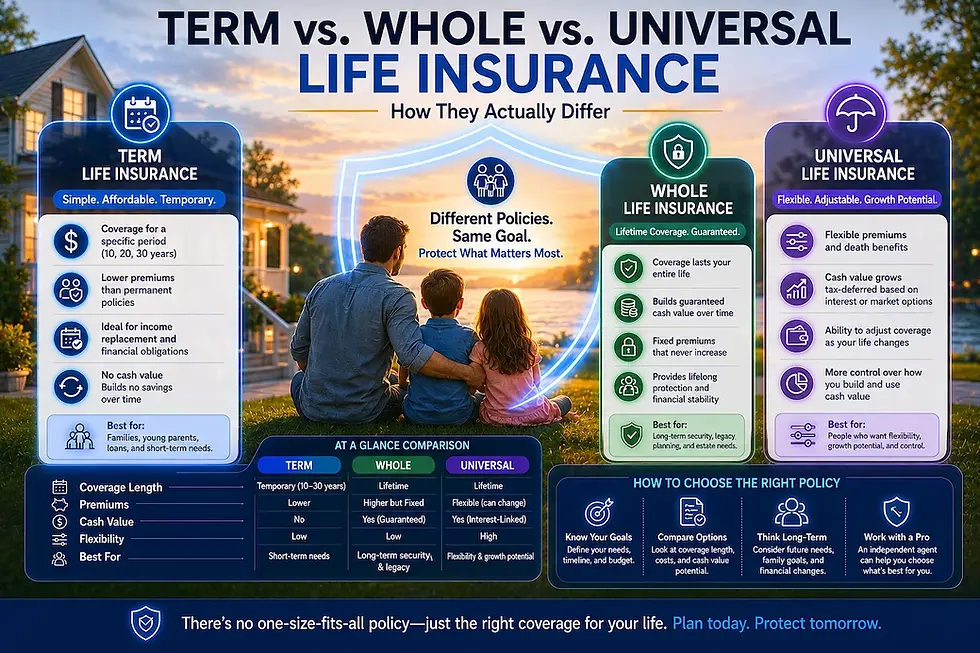

Term life insurance is designed to provide coverage for a specific period, commonly 10, 20, or 30 years. Its primary appeal is affordability. For many households, term insurance is the only way to secure a meaningful death benefit during years when financial obligations are highest. Mortgages, childcare costs, education planning, and income replacement needs tend to peak during working years, which aligns naturally with term coverage.

Whole life insurance, by contrast, is permanent coverage intended to last for the insured’s lifetime as long as premiums are paid. It combines a death benefit with a cash value component that grows over time. This structure introduces complexity and long-term financial commitment, which affects how and when people choose it.

In real-world decision-making, income stability is often the first dividing line. Households with limited discretionary income tend to favor term insurance because it delivers protection without straining monthly budgets. The lower premium allows families to prioritize immediate needs while still addressing the risk of premature death.

Age also plays a central role. Younger buyers are more likely to choose term coverage because the cost difference between term and whole life is substantial early on. As people age and accumulate assets, some revisit permanent coverage as part of broader estate or legacy planning. This transition is often driven by changing priorities rather than dissatisfaction with term insurance.

Another factor is how people perceive permanence. Many individuals are uncomfortable committing to a policy they may need to pay into for decades. Others value the certainty of lifetime coverage and prefer knowing their policy will not expire. These preferences are psychological as much as financial, and they heavily influence decision-making.

Cash value is frequently misunderstood. While whole life policies build cash value, access to those funds typically involves loans or withdrawals that can affect the death benefit. People who choose whole life for cash value often do so because they value forced savings or long-term financial structure, not because they expect liquidity comparable to traditional investment accounts.

Financial literacy also shapes outcomes. People who are comfortable managing investments often prefer term insurance paired with separate savings or investment strategies. Those who prefer simplicity or guaranteed outcomes may lean toward whole life, even at a higher cost. Neither approach is inherently superior; they reflect different comfort levels with risk and complexity.

Family structure matters as well. Parents with young children often prioritize maximum coverage at the lowest cost, favoring term insurance. Individuals without dependents may view permanent coverage as unnecessary, while those with long-term dependents or estate planning goals may see value in lifelong protection.

Another overlooked consideration is policy persistence. Term insurance is frequently allowed to lapse once financial obligations decrease. Whole life policies, once established, tend to remain in force longer due to accumulated cash value and sunk costs. This behavioral reality affects how policies function over decades, not just at purchase.

Sales framing can influence decisions, but it is rarely the sole driver. Most people ultimately choose based on what fits their current life stage. The same individual may reasonably choose term insurance at one point and whole life later, without either decision being a mistake.

Understanding how people actually decide between term and whole life insurance reframes the conversation. The choice is not about winning an argument, but about aligning coverage with evolving financial realities. Life insurance works best when it adapts to life stages rather than being treated as a one-time, permanent verdict.

Check out our Amazing!

Comments