Why Home Insurance Coverage Gaps Are More Common Than People Think

- Walter. J

- Dec 20, 2025

- 3 min read

Many homeowners assume that having an active insurance policy means their home is fully protected. In reality, coverage gaps are one of the most common and least understood problems in homeowners insurance. These gaps often remain invisible until a claim is filed, at which point homeowners discover that certain losses are limited, partially covered, or excluded altogether. Understanding why these gaps exist requires looking beyond marketing language and into how policies are structured.

Home insurance is not designed to cover every possible loss. Policies are written around defined risks, limits, exclusions, and conditions. Coverage gaps occur when a homeowner’s expectations do not align with those contractual boundaries. This misalignment is rarely the result of negligence; it is usually the product of assumptions made at purchase and policies that remain unchanged as homes and lifestyles evolve.

One of the most common sources of coverage gaps is dwelling coverage limits. Many homeowners focus on the market value of their home rather than the cost to rebuild it. Insurance, however, is based on reconstruction cost, not resale price. Changes in labor costs, building materials, and local construction codes can cause rebuilding expenses to rise faster than homeowners realize. If coverage limits are not updated periodically, a significant gap can develop between insured value and actual replacement cost.

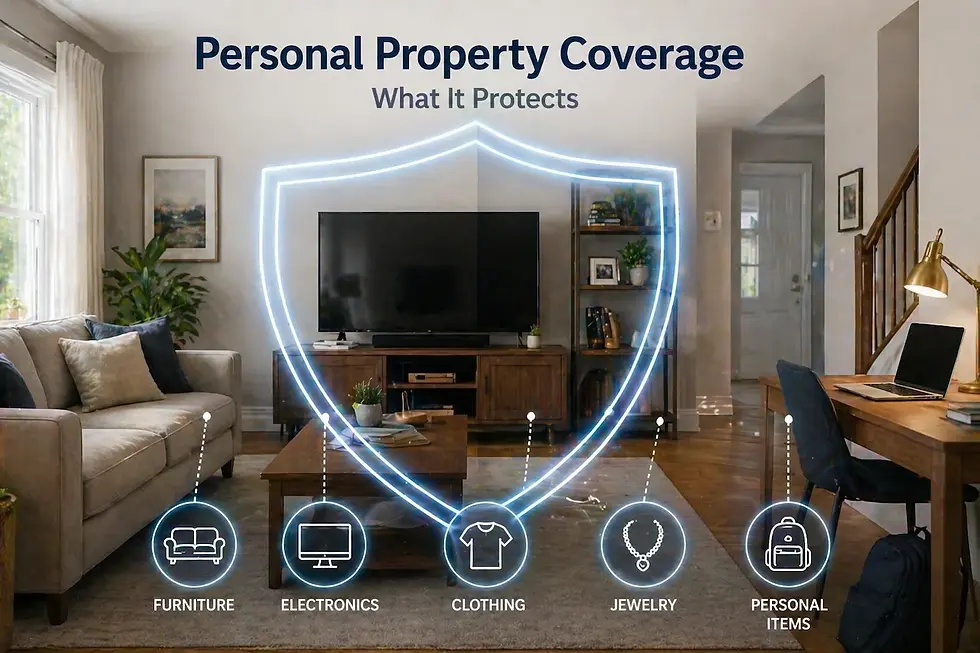

Another frequent gap involves personal property coverage. Standard policies apply limits based on a percentage of the dwelling coverage, but this does not guarantee full protection for all belongings. High-value items such as jewelry, electronics, collectibles, or specialized equipment may exceed sub-limits within the policy. Homeowners often discover these limits only after a loss, when reimbursement falls short of replacement needs.

Water damage is a particularly common area of confusion. While sudden and accidental water damage may be covered, long-term seepage, gradual leaks, or maintenance-related issues are often excluded. Homeowners may assume all water-related losses are treated the same, but policy language draws clear distinctions that significantly affect claim outcomes.

Natural disasters also contribute to coverage gaps. Floods and earthquakes are typically excluded from standard homeowners policies and require separate coverage. Homeowners who live outside high-risk zones may mistakenly believe these events are covered, only to find otherwise after a loss. Geographic risk does not eliminate exposure, and assumptions based on past experience can be misleading.

Loss of use coverage, which helps pay for temporary living expenses when a home is uninhabitable, is another area where gaps appear. Coverage limits and reimbursement rules vary, and many homeowners underestimate how quickly temporary housing, meals, and transportation costs can add up during extended repairs.

Policy exclusions related to wear and tear, neglect, and gradual deterioration are often misunderstood. Insurance is intended for sudden and unexpected events, not predictable aging or deferred maintenance. When damage is attributed to long-term conditions rather than a specific incident, coverage may be denied even if the result feels sudden to the homeowner.

Renovations and home improvements can unintentionally create gaps. Additions, finished basements, upgraded kitchens, and structural changes increase reconstruction costs, but policies do not automatically adjust to reflect these upgrades. Without periodic review, homeowners may be insuring yesterday’s version of their home.

Liability coverage gaps are also common. Standard liability limits may be insufficient in an environment where lawsuits and medical costs continue to rise. Homeowners often focus on property protection and overlook personal liability exposure, which can exceed policy limits in serious incidents.

Another overlooked gap involves ordinance or law coverage. After a major loss, local building codes may require upgrades that were not part of the original structure. Without adequate ordinance or law coverage, homeowners may be responsible for these additional costs out of pocket.

Coverage gaps persist because insurance policies are rarely reviewed once they are in place. Many homeowners renew year after year without reassessing limits, endorsements, or exclusions. Life changes such as acquiring valuable property, working from home, or hosting short-term guests can materially alter risk without triggering automatic policy updates.

Claims often serve as the first real test of coverage adequacy. When gaps are discovered during a claim, they can feel personal and unfair, even though the policy is functioning as written. Understanding these gaps before a loss occurs allows homeowners to make informed adjustments rather than reactive decisions.

Home insurance works best when expectations match reality. Coverage gaps are not failures of insurance, but reminders that policies are tools that require periodic review. Recognizing where gaps commonly occur empowers homeowners to align coverage with actual risk and avoid unpleasant surprises when protection is needed most.

Check out our Amazing!

Comments