Mobile Home Insurance Explained: How Coverage Works for Manufactured Homes

- Walter. J

- Jan 31

- 3 min read

Mobile homes face a different set of risks than traditional site-built homes, which is why standard homeowners insurance often isn’t designed to cover them. While mobile homes can provide affordable and flexible housing, they typically require a specialized insurance policy.

This guide explains how mobile home insurance works in the U.S., what it usually covers, what it doesn’t, and how it differs from standard homeowners insurance.

What Mobile Home Insurance Is

Mobile home insurance is designed for manufactured homes, including older mobile homes and newer manufactured housing built to federal standards.

These policies are often referred to as manufactured home insurance or mobile home insurance, and they’re tailored to the unique construction, mobility, and risk profile of these homes.

Unlike standard homeowners insurance, mobile home policies account for factors such as transportability, anchoring systems, and increased exposure to weather-related damage.

How Mobile Home Insurance Differs From Homeowners Insurance

The primary difference lies in construction and risk.

Traditional homeowners insurance is written for permanent, site-built homes.

Mobile home insurance is written for factory-built homes that may be relocated and often have different structural characteristics.

Because mobile homes are generally more vulnerable to wind, storms, and fire, insurers evaluate them differently and use policy forms designed specifically for manufactured housing.

What Mobile Home Insurance Typically Covers

While coverage varies by insurer and policy, mobile home insurance usually includes several core protections.

Dwelling Coverage

This covers the structure of the mobile or manufactured home itself, including:

Walls and roofing

Built-in appliances

Flooring and cabinetry

Attached structures, such as decks or porches (if included)

Coverage amounts should reflect the cost to repair or replace the home, not its market value.

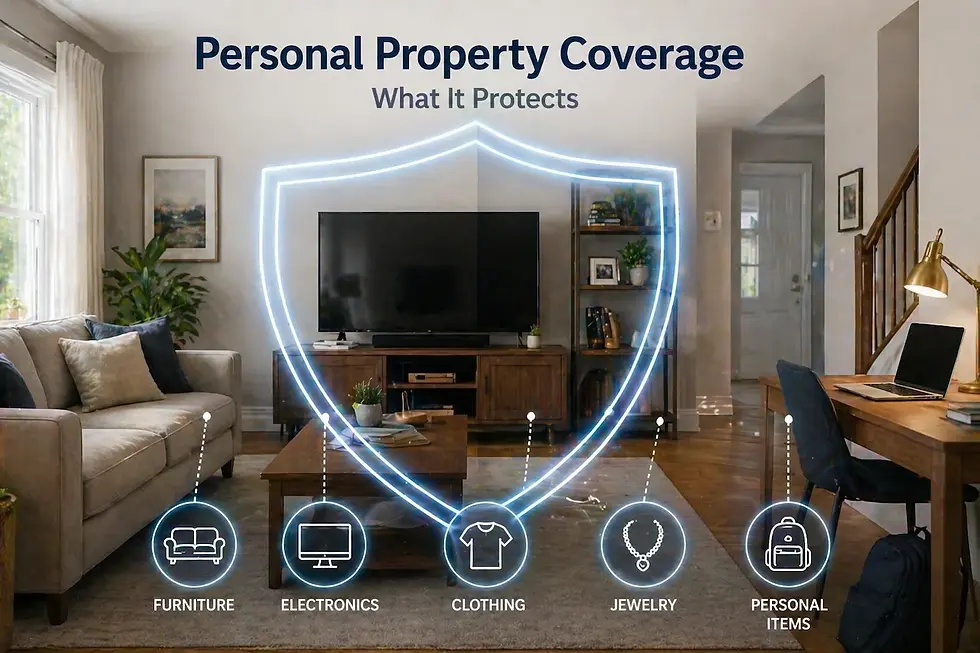

Personal Property Coverage

This protects personal belongings inside the home, such as:

Furniture

Clothing

Electronics

Household items

Coverage is typically provided for losses caused by covered events like fire, theft, or certain types of weather damage.

Personal Liability Coverage

Liability coverage helps protect the homeowner if someone is injured on the property or if the homeowner accidentally causes damage to someone else’s property.

Loss of Use Coverage

If the home becomes uninhabitable due to a covered loss, loss of use coverage may help pay for temporary housing and additional living expenses.

What Mobile Home Insurance Usually Does Not Cover

Mobile home insurance policies have exclusions and limitations that homeowners should understand.

Common exclusions include:

Flood damage (requires a separate policy)

Earthquake damage (requires separate coverage)

Wear and tear or maintenance issues

Certain wind or storm-related losses in high-risk areas

Older homes or homes not properly anchored may also face coverage restrictions or higher premiums.

Factors That Can Affect Mobile Home Insurance

Several factors influence coverage availability and cost, including:

Age of the home

Construction standards

Location and weather exposure

Anchoring and foundation type

Claims history

Some insurers may require inspections or upgrades before offering coverage.

Common Misunderstandings About Mobile Home Insurance

Mobile home owners often assume:

Their home qualifies for standard homeowners insurance

Market value determines coverage needs

Moving the home eliminates the need for insurance

In reality, mobile home insurance is specifically designed to address risks that standard homeowners policies do not cover well.

Key Takeaways for Mobile Home Owners

Mobile homes usually require specialized insurance

Standard homeowners insurance may not apply

Coverage should reflect replacement costs, not resale value

Flood and earthquake coverage are typically separate

Proper anchoring and maintenance can affect coverage

Mobile home insurance helps protect a type of housing that faces unique risks — and requires equally unique coverage.

Check out our Amazing!

Comments