Personal Property Coverage: How Homeowners Insurance Protects What You Own

- Walter. J

- Jan 29, 2025

- 4 min read

When homeowners think about insurance, the focus is usually on the structure of the house. Walls, roofs, and foundations feel tangible and permanent. Personal property, by contrast, often fades into the background — even though it may represent a large portion of a household’s financial value.

Personal property coverage exists to protect the items you own inside and around your home. Furniture, clothing, electronics, appliances, and countless everyday belongings fall under this category. Yet many homeowners do not fully understand how this coverage works until they are forced to inventory what they have lost.

By then, misunderstandings can be costly.

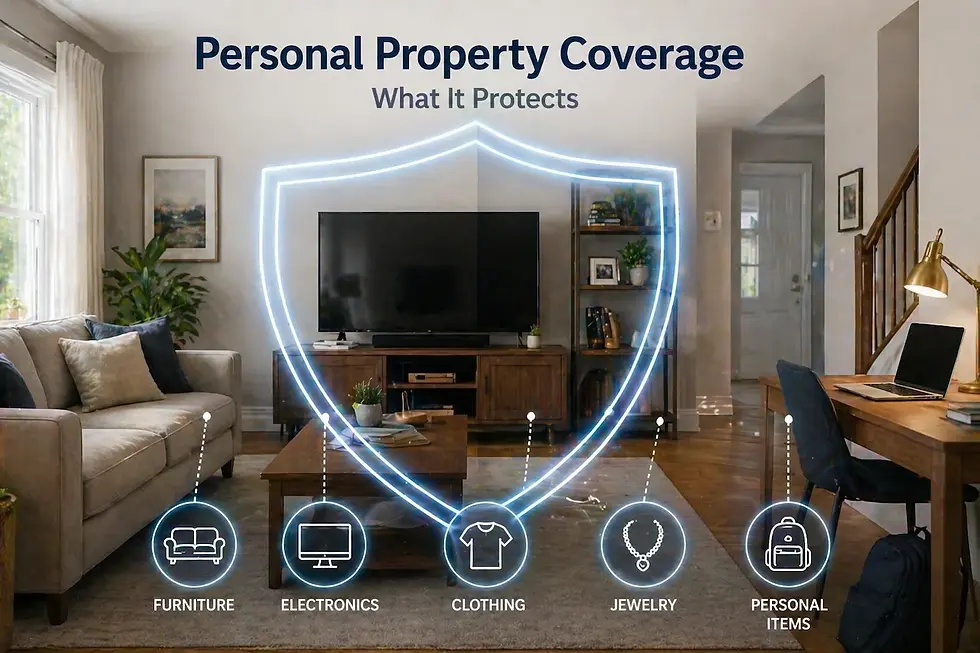

What Counts as Personal Property

Personal property includes the belongings you would take with you if you moved. This broad category covers items inside the home, in storage areas, and sometimes even property temporarily away from the house.

Common examples include:

Furniture and home furnishings

Clothing and personal items

Electronics and appliances

Kitchenware and household goods

Coverage often extends beyond the physical home itself. If personal property is stolen from a vehicle or damaged while traveling, certain policies may still apply, subject to limits.

The defining factor is ownership, not location.

How Coverage Limits Are Set

Personal property coverage is usually calculated as a percentage of the dwelling coverage limit. Many policies default to covering personal property at a set portion of the home’s insured value.

This method simplifies underwriting but does not account for lifestyle differences. Two homes with identical structures can contain vastly different amounts of personal property.

As a result, default limits may be insufficient for households with high-value furnishings, extensive wardrobes, or technology-heavy setups.

Replacement Cost vs. Actual Cash Value

One of the most important distinctions in personal property coverage is how losses are valued.

Actual cash value coverage factors in depreciation. Items are reimbursed based on their current value, not what it would cost to buy them new. Over time, this can significantly reduce claim payouts.

Replacement cost coverage, by contrast, reimburses the cost of replacing items with new ones of similar quality. While policies with replacement cost coverage may have higher premiums, they offer far more realistic protection in the event of a major loss.

Many homeowners assume replacement cost is standard. It often is not.

Why Personal Property Losses Add Up Quickly

After a fire, theft, or severe storm, homeowners are often surprised by how quickly personal property losses accumulate. Individual items may not seem expensive on their own, but collectively they represent substantial value.

Rebuilding a wardrobe, replacing electronics, and refurnishing a home can cost tens of thousands of dollars. Even modest households may discover their belongings are worth far more than anticipated.

This gap between perception and reality is one of the most common sources of underinsurance.

Special Limits on Certain Items

While personal property coverage is broad, it is not unlimited. Most policies impose sub-limits on specific categories of items.

Jewelry, watches, firearms, collectibles, and certain electronics often have coverage caps that apply regardless of the overall personal property limit. These caps are designed to manage risk but can surprise homeowners who assume all items are covered equally.

High-value items may require additional coverage or scheduling to ensure adequate protection.

How Claims Are Evaluated

Personal property claims often involve detailed documentation. Insurers typically require proof of ownership, descriptions, and approximate values. In large losses, adjusters may rely on inventories to assess claims.

This process can be stressful when records are incomplete or nonexistent. Homeowners who have never documented their belongings may struggle to recall everything they owned.

Maintaining a basic inventory, even a simple list or photo record, can make a significant difference.

Coverage Outside the Home

Personal property coverage is not limited to items physically inside the house. Many policies extend limited protection to belongings taken outside the home, such as luggage, laptops, or sports equipment.

These extensions are subject to policy terms and may have lower limits. Still, they provide an added layer of protection for property that moves with you.

Understanding these nuances helps set realistic expectations.

Why Personal Property Coverage Is Often Underestimated

Personal property coverage tends to be undervalued because belongings accumulate gradually. Items purchased over years rarely feel like a single investment, yet together they represent substantial financial exposure.

Homeowners may also assume that insurance automatically “keeps up” with their lifestyle. In reality, policies do not adjust unless prompted.

Periodic reviews help ensure coverage remains aligned with what you actually own.

Making Informed Adjustments

Adjusting personal property coverage is often straightforward. Increasing limits or switching to replacement cost coverage may have a relatively small impact on premiums compared to the protection gained.

The goal is not to insure every item perfectly, but to avoid large gaps that could create financial strain after a loss.

Personal property coverage works best when it reflects real-world living, not default assumptions.

Seeing Coverage for What It Is

Personal property coverage is about preserving normalcy after disruption. It allows homeowners to replace what was lost and continue life without starting from scratch financially.

Understanding how this coverage works — and where its limits lie — makes it easier to rely on it when it matters most.

For many homeowners, it is the quiet backbone of their insurance policy, protecting the things that make a house feel like home.

Important Note

This article is for informational purposes only and should not replace the terms of your actual insurance policy.

Written by Walter J., insurance research contributor focused on homeowners insurance at Insurance Policy Authority.

Like what you see here? Then...

Check out our Amazing!

Comments