Disclaimer: We share general insurance tips and insights — not licensed advice. Always check with a qualified insurance professional before making decisions. See full Disclaimer.

Insurance Policy Authority

Insurance advice for auto, home, and life.

Homeowners Insurance: Endorsements, Notes & Comparing Offers

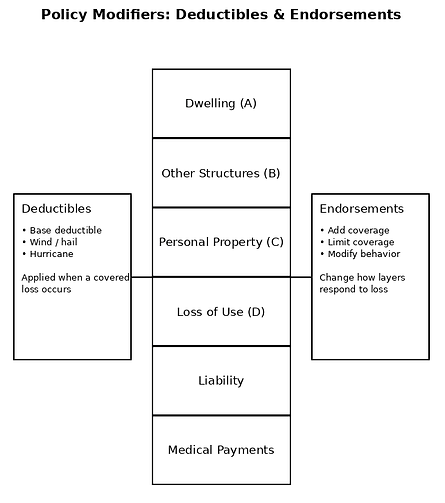

Endorsements & Add-Ons

(OCT Section 6)

Endorsements and add-ons modify a standard homeowners policy. They can strengthen coverage, limit it, or fill gaps that the base policy does not address.

This section is where policies that appear similar often differ the most.

What Endorsements Actually Do

An endorsement can:

-

Add coverage that is otherwise excluded

-

Increase limits for specific property

-

Change how losses are valued

-

Modify deductibles or conditions

Endorsements are not automatically good or bad. Their value depends entirely on:

-

What risk they address

-

How they interact with the rest of the policy

Common Endorsements to Review

When completing the OCT, note whether the following are included, excluded, or optional:

-

Ordinance or Law Coverage

Helps pay for increased rebuilding costs due to updated building codes after a covered loss.

-

Water or Sewer Backup

Covers damage caused by backed-up drains or sump pump failure, which is often excluded from base policies.

-

Scheduled Personal Property

Provides higher limits and broader coverage for valuable items such as jewelry, collectibles, or equipment.

-

Flood or Earthquake Coverage

Usually provided through separate policies or endorsements and excluded from standard homeowners insurance.

These endorsements often explain why one policy costs more — or why a cheaper policy leaves meaningful gaps.

Why This Section Matters

Endorsements determine whether a policy fits your specific home and risks, not just an average scenario.

Ignoring this section often leads to coverage surprises, especially after losses involving water damage, code upgrades, or high-value personal property.

This section ensures policy differences are visible before they matter.

Notes, Red Flags & Comparing Offers

Not every important detail fits neatly into a coverage box.

The Notes and Red Flags section exists to capture:

-

Exceptions

-

Unclear language

-

Agent explanations

-

Anything that feels unusual or inconsistent

What to Write Down

Use this space to note:

-

Verbal assurances not clearly reflected in writing

-

Coverage that depends on conditions or interpretation

-

Differences in how agents describe “similar” coverage

-

Gaps that may require follow-up questions

This section legitimizes careful evaluation.

If something feels unclear, it usually is.

Getting Homeowners Insurance Quotes

At this point in the guide, you should understand how homeowners insurance is structured, what each coverage does, and how policies can behave very differently despite similar pricing.

This is where shopping for quotes makes sense.

Getting homeowners insurance quotes is not about finding the lowest number. It’s about gathering complete offers so you can evaluate how each policy is built and how it would respond during a real loss.

Many people start this process too early, before they understand what they are comparing. You now have the context to do it correctly.

How to Approach the Quote Process

When requesting homeowners insurance quotes, focus on structure first, price second.

Ask for:

-

A complete policy quote, not just a premium estimate

-

Clear coverage limits for dwelling, personal property, and liability

-

Deductible details for different types of losses

-

Any endorsements or exclusions that materially affect coverage

If a quote cannot be clearly explained or documented, it is not ready to be compared.

Using the Offer Comparison Tool While Getting Quotes

This guide is designed to be used alongside the Homeowners Offer Comparison Tool (OCT).

As you receive quotes:

-

Use one page per insurance offer

-

Record the coverage details exactly as presented

-

Do not rely on verbal summaries or assumptions

Filling out the tool as quotes arrive prevents price-only decisions and makes differences between policies easier to see.

You do not need dozens of quotes.

In most cases, two to three complete offers are enough to make an informed decision.

Asking About Discounts and Bundling

Once you understand the coverage being offered, it’s reasonable to ask about ways to reduce premium without weakening protection.

Common topics to discuss include:

-

Bundling homeowners and auto insurance

-

Home safety or security features

-

Claims-free or loyalty discounts

Discounts should be evaluated after coverage is set. Reducing price by removing meaningful protection often costs more in the long run.

Why Homeowners Quotes Vary So Much

It’s common for homeowners insurance quotes to differ significantly, even for the same property.

This usually happens because:

-

Coverage limits are calculated differently

-

Valuation methods vary

-

Deductibles are structured differently

-

Endorsements and exclusions are not the same

Large price differences are a signal to slow down and compare structure, not a signal that one offer is automatically better.

When You’re Ready to Compare Offers

Once you’ve collected complete quotes and filled out the Offer Comparison Tool, you’re ready to evaluate them properly.

This final step isn’t about finding a perfect policy. It’s about choosing coverage that:

-

Matches your property and location

-

Aligns with your risk tolerance

-

Behaves predictably during real losses

The next section explains how to compare completed offers side by side and make a confident homeowners insurance decision.

Comparing Offers Correctly

Once each offer has its own completed OCT page, comparison becomes much easier.

Instead of asking:

“Which policy is cheaper?”

You can ask:

-

Which policy protects the structure best?

-

Which handles displacement realistically?

-

Which exposes me to the least out-of-pocket risk?

-

Where do coverage scopes differ?

-

Which exclusions matter most for my situation?

Price should be evaluated last, not first.

Why Three Offers Is Enough

Comparing more than three policies often:

-

Creates diminishing returns

-

Increases confusion

-

Encourages over-optimization

Three well-documented offers are usually sufficient to identify:

-

Outliers

-

Tradeoffs

-

Meaningful differences

The goal is clarity, not volume.

Making an Informed Homeowners Insurance Decision

By this point, you should understand:

-

What each policy covers

-

How it behaves during losses

-

Where limits, deductibles, and exclusions differ

-

Why premiums are different

At this stage, the “right” policy is not the cheapest one — it’s the one that:

-

Aligns with your risk tolerance

-

Matches your property and location

-

Behaves predictably during real claims

Homeowners insurance decisions are rarely about perfection.

They are about making tradeoffs knowingly instead of accidentally.

Final Thought

Most homeowners don’t regret buying insurance.

They regret discovering how it works after they needed it.

This guide and the Offer Comparison Tool exist to prevent that outcome.

Homeowners insurance can be difficult to evaluate without clear structure and context. Our goal with this guide was to provide both — straightforward explanations and practical tools that help you understand how coverage works, how policies differ, and how to compare offers more confidently.

If this guide helped clarify homeowners insurance for you, you may also find value in our other insurance guides below:

-

Auto Insurance Guide — focused on understanding coverage, limits, pricing, and real-world claim behavior.

-

Life Insurance Guide — designed to explain coverage types, decision factors, and long-term considerations without sales pressure.

Each guide is built to support informed decision-making, not to promote specific products. Use the resources that are relevant to you, and revisit them whenever your insurance needs change.