Disclaimer: We share general insurance tips and insights — not licensed advice. Always check with a qualified insurance professional before making decisions. See full Disclaimer.

Insurance Policy Authority

Insurance advice for auto, home, and life.

Homeowners Insurance: Covered Perils, Coverage Scope & Deductibles

Covered Perils & Coverage Scope

(OCT Section 5)

Coverage limits tell you how much a policy can pay.

Perils and coverage scope determine when it will pay.

This section explains why many claim denials happen even when limits appear adequate.

Open Perils vs. Named Perils

Homeowners policies generally cover losses in one of two ways:

-

Open Perils (All-Risk)

Covers all causes of loss except those specifically excluded -

Named Perils

Covers only the causes of loss explicitly listed in the policy

This distinction applies separately to:

-

The dwelling

-

Personal property

For example, a policy may provide:

-

Open-peril coverage for the dwelling

-

Named-peril coverage for personal property

That difference has real consequences during a claim.

Why This Distinction Matters

With named-peril coverage:

-

The burden is often on the policyholder to show the loss is covered

-

Losses caused by unlisted events are excluded by default

With open-peril coverage:

-

The insurer must rely on exclusions to deny coverage

Two policies with identical limits can produce opposite outcomes depending on how perils are defined.

When filling out the OCT:

-

Record whether dwelling coverage is open or named peril

-

Record whether personal property coverage is open or named peril

Exclusions Are as Important as Coverages

Exclusions define what a policy will not cover, even if damage is severe.

Common exclusions include:

-

Flood

-

Earthquake

-

Wear and tear

-

Certain water-related losses

-

Neglect or deferred maintenance

Exclusions often explain why policyholders say:

“I thought I was covered for that.”

When reviewing offers:

-

Look for exclusions that affect your geographic area or home features

-

Note any exclusions that significantly narrow coverage

This section of the OCT is where you document those limitations.

Why This Section Matters

Coverage scope determines whether insurance responds at all.

A policy with lower limits but broader coverage may provide better real-world protection than a higher-limit policy with restrictive perils and exclusions.

This section ensures you evaluate coverage behavior, not just coverage size.

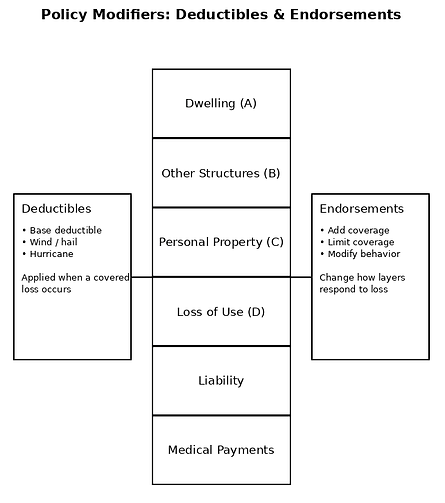

Deductibles by Event

Deductibles determine how much financial responsibility you retain when a loss occurs.

They do not change whether a loss is covered — they change how expensive the loss is for you.

Base Deductible

The base deductible applies to most covered losses.

A higher deductible:

-

Lowers premium

-

Increases out-of-pocket cost

A lower deductible:

-

Raises premium

-

Reduces out-of-pocket exposure

At this stage, the deductible should be evaluated alongside coverage limits, not in isolation.

Event-Specific Deductibles

Many homeowners policies include separate deductibles for specific events, such as:

-

Wind

-

Hail

-

Hurricanes

These deductibles may be:

-

Flat dollar amounts

-

Percentages of the dwelling limit

Percentage-based deductibles can result in significant out-of-pocket costs after a major loss.

When completing the OCT:

-

Record each deductible separately

Note whether it is flat or percentage-based

Why Deductibles Are Often Misunderstood

Deductibles are frequently misunderstood because:

-

They are discussed primarily as a pricing tool

-

Their real financial impact is not obvious until a claim occurs

Two policies with the same premium and limits can expose homeowners to very different costs due to deductible structure alone.

Why This Section Matters

Deductibles determine how much risk you retain, not how much insurance you buy.

Understanding deductibles by event prevents surprises at the worst possible moment — after a loss has already occurred.

This section ensures deductible decisions are intentional, not accidental.

What Comes Next

Only one section remains, and it completes the evaluation process:

-

Section 6: Endorsements, Notes & Comparing Offers