Disclaimer: We share general insurance tips and insights — not licensed advice. Always check with a qualified insurance professional before making decisions. See full Disclaimer.

Insurance Policy Authority

Insurance advice for auto, home, and life.

Auto Insurance: Coverage

This section is the most important part of this guide. Take your time and focus on understanding the concepts presented here, as they will directly impact the decisions you make when choosing your coverage.

If you're already familiar with the basic purpose of auto insurance and want to focus on understanding your coverage options, you can begin here. This section is designed to help you understand the major areas of protection available within a policy and how they work together.

So what exactly is coverage?

Auto insurance, as a service, is designed to provide protection. Coverage is how that protection is defined. It represents the specific areas you choose to protect and the types of protection applied to those areas.

If we think of insurance as a shield or safety net, then coverage determines how much of that shield you have, and what it is designed to protect.

At its core, coverage can be understood as:

Coverage = Areas + Types

To fully understand coverage, you must first understand the different areas that can be protected. Then, you must understand the types of coverage available for each of those areas.

Once these two pieces are clear, the rest of the process becomes much easier to follow.

There are many moving parts within a car insurance policy, and it can seem complex at first. To simplify this, we’ve created a structured visual framework that breaks coverage down into clear, manageable components.

(This framework describes areas of risk that exist across insurers and states. Policies may be written differently, but the underlying risks—and how coverage responds to them—are consistent.)

We begin by identifying the different areas of coverage.

Areas of Coverage

One of the most common misconceptions about car insurance is that it only protects your car. In reality, coverage extends beyond your vehicle to include multiple areas where damage or loss can occur.

To better understand this, we will think of coverage as a single, complete unit. For illustration purposes, we represent it as a full circle. From there, we break it down into smaller sections, each representing a specific area of protection.

To identify these areas, consider a simple scenario: you are involved in an accident with another vehicle.

From this situation, we can separate everything into two sides:

-

your side

-

the other party’s side

Within each side, there are two types of things that can be affected:

-

people

-

property

When combined, these create the four main areas of coverage.

(The sections shown above represent categories of risk, not equal importance, limits, or cost. The amount of coverage selected within each category can vary significantly.)

You

This area provides protection for you and the passengers in your vehicle, primarily covering medical expenses resulting from an accident.

Your Car

This area provides protection for your vehicle, covering damage from collisions and other qualifying events.

Other People

This area provides protection for individuals injured in an accident you cause. This may include other drivers, passengers, cyclists, or pedestrians.

Other Property

This area provides protection for property you damage in an accident you cause. This may include other vehicles, buildings, and public property such as light poles or fire hydrants.

Together, these four areas form the foundation of coverage in an auto insurance policy.

Now that we’ve identified the areas of protection, the next step is understanding the types of coverage that apply within each area.

Types of Coverage

Each coverage area includes specific types of protection. When a coverage type appears within an area, it applies to expenses related to that portion of your coverage. Below is an overview of how different coverage types provide protection within each area.

We now take a look at some of the most common coverage types and how they fit into the areas we identified earlier.

Personal Injury Protection (PIP)

Covers medical expenses for you and your passengers, regardless of who caused the accident (in applicable states).

Collision (Coll)

Covers damage to your car resulting from a collision with another vehicle, object, or from events such as a rollover.

Comprehensive (Comp)

Covers damage to your car that is not caused by a collision. This may include theft, fire, vandalism, falling objects, weather events, or contact with animals.

Bodily Injury Liability (BIL)

Covers medical expenses for other people if you cause an accident.

Property Damage Liability (PDL)

Covers damage you cause to other people’s property, including vehicles and structures.

Both Bodily Injury Liability (BIL) and Property Damage Liability (PDL) are collectively referred to as "Liability Coverage".

A note about "Full Coverage".

You may hear the term "full coverage" when shopping for auto insurance.

Full coverage is not a specific type of insurance. Instead, it is a commonly used term that generally refers to a policy that includes:

-

Liability Coverage

-

Collision Coverage

-

Comprehensive Coverage

Because the term is not formally defined, the exact protections included can vary. For that reason, it is usually more helpful to focus on the individual coverage types included in a policy rather than the label itself.

Together, these coverage types form the building blocks of your policy

These are some of the most common coverage types. Additional types may be available depending on your state and insurer. You can review our Coverage Type List to see the standard types of coverage available.

How Coverage is Structured when Sold

Insurance is built around money.

You pay the insurance company a set amount, and in return, the company agrees to pay for covered expenses up to certain limits.

When you review a policy, each coverage type is typically shown alongside a limit. This limit represents the maximum amount the insurance company will pay for that specific type of coverage.

There are two main ways these limits are structured:

-

limits you can choose

-

limits that are determined for you

We’ll start with the ones you can control.

For these, there are two common formats: single limits and split limits.

Single Limit

A single limit sets one maximum amount the insurance company will pay for a specific type of coverage per accident.

For example, if you have Property Damage Liability coverage with a $15,000 limit, this means the insurance company will pay up to $15,000 for damage you cause to other people’s property in a single accident.

The single-limit structure is straightforward: one coverage type, one maximum payout per accident.

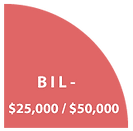

Split Limits

Split limits set separate maximum amounts for different parts of a claim.

They are most commonly used with Bodily Injury Liability coverage and are typically shown as two numbers:

-

a limit per person

-

a limit per accident

For example, a policy might show limits of $25,000 per person and $50,000 per accident.

The first number is the maximum amount the insurance company will pay for injuries to any one person.

The second number is the maximum total amount the company will pay for all injuries combined in a single accident.

Let’s walk through an example to see how these limits work in practice.

Let's say four people in another vehicle are injured in an accident you caused. One person has $30,000 in medical expenses, while the other three each have expenses of $5,000. The total comes to $45,000.

Even though the total is below the $50,000 per-accident limit, the insurance company will not pay the full $45,000.

This is because of the $25,000 per-person limit.

-

The first person’s $30,000 bill exceeds the per-person limit, so only $25,000 is covered.

-

The other three individuals each have $5,000 in expenses, which are fully covered.

This brings the total payout to $40,000.

Now let’s look at a different scenario.

Let's say four people are injured in another accident you caused, and each person has medical expenses of $15,000. The total comes to $60,000.

In this case, each individual expense is below the $25,000 per-person limit. However, the total exceeds the $50,000 per-accident limit.

Because of this, the insurance company will not pay the full $60,000.

Instead, the total payout is capped at $50,000 and must be distributed across all four individuals.

In this scenario, each person would receive $12,500, bringing the total payout to the $50,000 per-accident limit.

This illustrates how single limits and split limits are structured.

Limits You Cannot Choose

Not all coverage types allow you to select a limit.

For certain coverages—specifically Collision and Comprehensive—the maximum payout is not something you set. Instead, it is based on the value of your vehicle.

Unlike liability coverages, where you choose a fixed dollar limit, these coverages are tied to what your car is worth at the time of the loss.

Because your vehicle’s value changes over time (typically decreasing due to depreciation), there is no fixed limit shown in the same way as other coverage types.

If your car is totaled, the insurance company will pay the vehicle’s actual value at that time, subject to the terms of your policy.

Instead of selecting a limit, you will typically choose a deductible for these coverages.

The deductible is what you are responsible for paying before the insurance company covers the remaining cost.

Deductibles

Collision and Comprehensive coverage use what is called a deductible.

A deductible is the amount you must pay out of pocket before the insurance company pays the remaining cost of a covered claim.

In simple terms, you share part of the cost before the insurance coverage applies.

In a straightforward scenario, you might expect that if your car is damaged, the insurance company would simply pay to fix it. However, before the insurance company pays anything, the deductible must first be satisfied.

For example, if you have a $500 deductible and your car is damaged in an accident resulting in $1,200 in repair costs:

-

You pay the first $500

-

The insurance company pays the remaining $700

If the total cost of repairs is less than your deductible, then the insurance company does not pay anything.

For example, if the damage totals $400 and your deductible is $500, you would pay the full $400 out of pocket, and there would be no reason to file a claim.

A claim is the formal process of reporting damage to your insurance company and requesting payment for a covered loss.

You would typically file a claim only when the cost of damage exceeds your deductible.

It’s important to understand that the deductible applies each time you file a claim for damage to your vehicle.

In many cases, this applies regardless of who was at fault, depending on how the claim is handled.

You can choose your deductible amount.

In general:

-

higher deductibles result in lower premiums

-

lower deductibles result in higher premiums

This is because you are taking on more or less of the financial risk.

When purchasing Collision and Comprehensive coverage, instead of seeing a typical limit amount listed after the coverage type, you’ll see the deductible amount.

This gives you a clearer view of how common coverage types are structured.

These four areas—coverage types and their corresponding limits—make up your core coverage. This diagram is also referred to as your coverage chart.

Now that you understand how coverage is structured, the next step is understanding how it works in practice.

The two Auto Insurance Systems used by States

Auto insurance policies generally fall into two systems: at-fault and no-fault.

At-Fault Auto Insurance

In an at-fault (or tort) system, the driver who caused the accident is financially responsible for the damages. After an accident, fault is determined, and the at-fault driver’s insurance pays for injuries and property damage suffered by others.

Most U.S. states follow this system. Under this structure, liability coverage plays a central role, as it protects you if you cause harm to other people or their property.

No-Fault Auto Insurance

In a no-fault system, each driver’s own insurance pays for certain expenses—typically medical costs—regardless of who caused the accident. This allows for faster access to benefits and can reduce the need for lawsuits.

However, fault is not entirely removed. In more serious situations, or depending on state rules, fault may still determine whether additional claims or legal action are allowed.

Why This Matters:

Understanding which system your state follows helps you interpret how your coverage works in practice. It affects how claims are paid, what protections are most important, and why certain coverages may be required.

State Minimum Coverage Requirements

In most states, auto insurance is required by law. If it is required where you live, there is also a minimum amount of coverage you must carry.

These minimum requirements are set by the state and typically define:

-

the types of coverage you must have

-

the minimum limits for those coverages

The exact requirements vary by state.

Before viewing the list below, it’s important to understand how to read the visual format used in the state breakdowns:

-

Mandatory coverage, is shown inside a solid-colored area with the coverage name highlighted in bold white text. This means it is legally required in that state.

-

Must be offered / can be declined coverage, is shown in a lighter grey text. This means the insurer must offer it, but you may reject it (in writing). While not technically part of the mandatory state minimum, these coverages are included in the illustration because you will see them when shopping for auto insurance.

This system is designed to let you quickly see the minimum coverage requirements in your state.

Below is a list of all states. Select your state to view its minimum coverage requirements.

State Minimum List

(Minimum coverage requirements and certain coverages that can be declined vary by state and may change over time. Some coverages may require a written rejection. Last reviewed: May 2026. Always verify requirements with your state or insurance provider.)

You should also review the Coverage Type List to understand the different types of coverage available for each area. Although coverage for a particular area may not be required in your state, it is helpful to be aware of the available protection in case you decide to add it.

Meeting the state minimum only keeps you legally compliant. It does not necessarily mean you are adequately protected.

In many cases, the minimum required coverage may not be enough to fully cover the cost of a serious accident.

Choosing the Right Amount of Coverage

Now that you understand how coverage is structured and the minimum required in your state, the next step is deciding how much coverage you actually need beyond that baseline.

This is one of the most important decisions you will make when selecting an auto insurance policy.

To help guide that decision, we start by looking at what is at risk in each area of coverage.

For the area that protects you, what’s at stake is your health and the well-being of your passengers. Without adequate coverage, medical treatment may become a financial burden.

For your vehicle, what’s at stake is your mobility. If your car is damaged or totaled, your ability to carry out daily responsibilities may be affected.

For the areas that protect others (liability coverage), what’s at stake is your financial stability. You are responsible for damages you cause to other people and their property. Without sufficient coverage, these costs may need to be paid out of your own assets.

Understanding what is at risk allows you to make more informed decisions about how much protection you need in each area.

Next, we review the industry-recommended limit amounts for each coverage area. These amounts are generally believed to provide sufficient protection for most people.

However, it’s important to take the time to determine the coverage levels that are right for you rather than relying solely on these recommendations. Think of them as a guideline to help inform your decision. Depending on your personal needs, you may require more or less coverage than the industry-recommended amounts.

There is no exact formula for choosing the right coverage amounts.

The severity of future accidents cannot be predicted, and no one can determine the exact level of protection you will need.

Because of this, the goal is not to find a perfect number, but to make a well-informed decision based on your situation, priorities, and financial comfort.

Building Your Coverage

To choose the right amount of coverage, we’ll walk through a simple step-by-step process.

The goal is to build a coverage structure that reflects what matters most to you and provides a level of protection you are comfortable with. Open or print out a copy of the Blank Coverage Chart.

Step 1: Start with Required Coverage

Begin by identifying the coverage types required in your state. These are the ones you must include in your policy to remain legally compliant.

Use your state’s minimum requirements as a reference and make sure these coverage types are included in your plan.

Step 2: Add Other Standard Coverage (If Needed)

Next, consider whether there are other standard coverage types you would like to include.

These are not required, but they can provide valuable protection depending on your situation. Review the standard coverage types and select any that you feel are important to you.

At this point, you should have a list of coverage types that will make up your core coverage.

Step 3: Choose Your Coverage Limits

Now, determine how much protection you want for each coverage type.

When choosing limits, focus on the two main areas of risk:

-

protection for people

-

protection for property

For people, consider the potential cost of medical treatment. Think about a scenario where multiple individuals are injured and ask yourself whether your coverage would be sufficient to handle those expenses.

For property, consider both your vehicle and the property of others.

-

For your vehicle, think about whether you can afford your deductible if damage occurs, possibly more than once.

-

For other people’s property, consider the value of vehicles and structures in the areas where you typically drive.

The goal is not to predict the exact cost of a future accident, but to choose limits that provide a reasonable level of protection based on your situation.

Once completed, you will have a personalized coverage structure that reflects your needs and priorities.

This becomes your personal coverage blueprint.

Extra Coverage

In addition to your core coverage, there are optional coverages that can be added to your policy for extra protection.

These coverages are not required, but they may be useful depending on your situation.

Below are some of the most common optional coverage types:

Rental Reimbursement

Covers a portion of the cost of a rental car while your vehicle is being repaired due to a covered loss. Policies typically include daily and total limits. Availability and structure may vary by state and insurer.

Towing Coverage (Roadside Assistance)

Covers certain costs if your vehicle becomes disabled. This may include towing, lockout assistance, or other roadside services.

Guaranteed Asset Protection (GAP) Insurance

Helps cover the difference between what you owe on your vehicle and its actual value if it is totaled. This is most relevant for vehicles with loans or leases.

These are some of the most common optional coverages, but others may be available. Coverage names and details can vary by insurance company, even when the protection offered is similar.

Adding extra coverage will typically increase your premium, so consider the value of each option before including it in your policy.

Common Mistakes (FYI)

Before moving forward, it’s worth pointing out a few common mistakes people make when choosing coverage. Being aware of these can help you avoid costly decisions and better understand how to approach your options.

-

Choosing minimum coverage only based on price (priority mistake)

A common mistake when choosing coverage is focusing only on price and selecting the minimum required amounts without considering what is actually at risk. While minimum coverage may reduce cost upfront, it may not provide enough protection in more serious situations. The goal is to find a balance between affordability and meaningful protection.

-

Not understanding deductibles (mechanics mistake)

Some people choose higher deductibles to lower their premium without fully considering whether they can afford to pay that amount out-of-pocket when needed. A deductible should always be an amount you can realistically afford at any time.

-

Assuming “full coverage” means everything (definition mistake)

The term “full coverage” is commonly used but has no fixed definition. It typically includes a combination of coverages, but it does not mean every situation is covered. Always review your actual coverage types and limits to understand what is and isn’t protected.

That concludes this section on coverage.

At this point, you should have a clear understanding of how coverage is structured, how it is applied, and how to choose an amount that fits your needs.

You’ve seen how coverage is built around different areas of risk, how specific coverage types provide protection within those areas, and how limits and deductibles determine the level of protection you receive.

With this foundation in place, the next step is to understand how pricing works.

In the next section, we’ll break down the factors that affect the cost of auto insurance and show you how to evaluate and compare different offers.